by Ali Rind, Last updated: July 16, 2026

.webp)

A single insurance claim rarely stays inside one organization. By the time it closes, the file has usually passed through an adjuster, often a third-party administrator, a medical reviewer, a repair or estimate vendor, outside legal counsel, and sometimes a reinsurer, an investigator, or a regulator. Each handoff moves the claim toward resolution. It also moves policyholder data into systems the carrier does not control and cannot directly monitor.

The detail that gets overlooked is that accountability does not travel with the file. When a vendor exposes policyholder information, the carrier that shared it remains answerable under the regulations governing insurance data. A breach at a small medical-review firm becomes the carrier's regulatory problem, the carrier's notification obligation, and the carrier's reputational damage. That is what turns redaction from a clerical step into a third-party risk control the carrier owns, applied at the moment data is about to leave its environment.

This article looks at where policyholder data is most exposed across the vendor network, what US regulators expect when that data changes hands, why the usual governance stack misses the files that matter most, and how redaction closes the gap before a file is ever shared.

The vendor network is where policyholder data is most exposed

Insurance is a collaborative business by design. A claim resolves faster when an adjuster, an investigator, a medical reviewer, and an analytics team can each work from the same evidence. The cost of that speed is a steadily widening exposure surface, because every party added to a claim brings its own systems, storage, retention habits, and staff who can copy, forward, or misfile a document.

It helps to be concrete about who receives what. A third-party administrator handling claims intake sees full policyholder identity and loss details. A medical reviewer on an injury claim works with protected health information. An independent adjuster or estimator receives photographs and video of the scene, which routinely capture bystanders, license plates, and the interior of someone's home. Outside counsel preparing for litigation gets the complete file, including recorded statements.

A reinsurer assessing exposure needs the accident narrative and the financials. A data analytics or fraud-detection vendor may ingest thousands of files at once. Each of these relationships is legitimate and necessary. Each is also a separate point where a privacy failure can occur, and the carrier carries the consequence of all of them.

The material that flows through this network is mostly unstructured. It lives in scanned loss reports, medical records, settlement letters, recorded calls, dashcam and surveillance footage, and accident photographs, not in tidy database fields. These are the formats that are hardest to track once shared and, inconveniently, the formats vendors most need to do their work.

Video is the sharpest example, because a property or auto claim often hinges on footage that shows uninvolved people alongside the relevant evidence. Sharing it safely means removing the people who are not part of the claim, which is the problem our guide to video redaction for insurance claims was written to solve.

What US regulators expect when data leaves your control

Insurers in the United States sit under several overlapping regimes, and the consistent theme across all of them is that responsibility extends to vendors.

The Gramm-Leach-Bliley Act applies to insurers as financial institutions, and its Safeguards Rule requires covered companies to maintain a written information security program and to take reasonable steps to ensure that their service providers protect customer information in their care. The obligation is explicit that the duty follows the data to the provider rather than ending at the carrier's firewall. The amended rule also introduced breach notification expectations, which raise the stakes on any exposure that originates in a vendor's environment.

The NAIC Insurance Data Security Model Law, commonly cited as Model 668, sets a parallel expectation at the state level. Licensees must develop and maintain an information security program, investigate cybersecurity events, and exercise due diligence in selecting and overseeing third-party service providers. A growing number of states have adopted it or enacted closely related laws, which means most national carriers now face this requirement somewhere in their footprint.

HIPAA applies whenever a claim involves protected health information, which is the norm in health, disability, and workers' compensation lines. Sharing that information with a reviewer or administrator brings business-associate obligations into play. State privacy laws led by California's CCPA and CPRA add another layer, with consumer rights and specific rules on how personal information is disclosed to and used by third parties.

There is a practical advantage folded into these frameworks that is easy to miss. When data is genuinely de-identified before it is shared, it frequently falls outside the definition of personal information that triggers the strictest obligations. Anonymization applied before a handoff does two things at once. It lowers the chance that a shared file causes harm, and it can narrow the regulatory scope of the data itself, since information that no longer identifies a person is treated differently under several of these laws. That is why redaction functions as a compliance accelerator instead of a tax on the workflow: the cleaner the file that leaves, the lighter the obligations that follow it.

Why the usual risk stack misses the files that matter

Most insurers already run some form of third-party risk management. Vendors are tiered, security questionnaires go out, SOC 2 reports are collected, and contracts include data-protection clauses. This machinery is valuable, and it is also aimed almost entirely at structured risk: the vendor's posture, certifications, and contractual commitments.

The claim files themselves sit outside that scope. A vendor can pass every assessment, hold every certification, and sign every clause, and still receive a document packed with unredacted Social Security numbers, medical details, and a clear view of a policyholder's front door. The governance stack assessed the vendor. It never inspected the file. That gap is where most real exposure lives, because the sensitive content moves in unstructured documents and recordings that the assessment process was never built to examine.

Closing it requires a control that operates on the content rather than the relationship. A contract clause expresses an intention about how a vendor should behave. Redacting the file before it leaves removes the carrier's dependence on that behavior entirely. If a sanitized document is later forwarded to the wrong inbox or left on an unmanaged device, the information that would have caused harm is already gone. The risk is addressed at the source instead of being transferred, on paper, to a third party.

Where claim data actually leaks

The distance between a written policy and daily practice is usually where exposure happens, and the failure points tend to be ordinary rather than dramatic.

Claim documents get emailed through channels never intended for sensitive data, because the deadline is now and the secure portal is slow. Files are downloaded to a laptop for a quick review and then forwarded without anyone stripping the identifiers. A full surveillance clip is sent to an external investigator in its entirety because trimming and blurring it by hand would take hours the adjuster does not have.

Different team members redact the same kind of document differently, so one file leaves clean while the next leaves with a policy number still visible in a header. A signed data processing agreement sits in a drawer assuming a vendor will be careful, but the agreement does not act at the moment a document is attached and sent.

Consider a routine workers' compensation claim. The file contains the claimant's identity, medical records describing the injury, a recorded statement, and surveillance footage gathered during the investigation. To move it forward, the carrier shares portions with a medical reviewer, an independent adjuster, and eventually outside counsel.

If each recipient receives the complete file, the claimant's protected health information and the faces of uninvolved people travel to three separate organizations, none of which the carrier monitors directly. If each recipient instead receives only what their role requires, with identities and unrelated parties removed, the same claim advances at the same speed with a fraction of the exposure. Adjusters sit at the center of this, since they assemble and send most of these packages, which is exactly the pressure our piece on redaction for insurance claim adjusters addresses.

Building redaction into the claims pipeline

Treating redaction as a control means putting it at the point in the workflow where data is about to leave, so the version going to a vendor is sanitized by default and the original stays protected internally. Three things make that practical at the volume insurers operate.

The first is format coverage. Claim evidence arrives as documents, scanned files that need optical character recognition to read text trapped in an image, photographs, video, and audio from recorded calls. A tool that handles only one of these formats leaves the rest to manual effort, and manual effort under deadline pressure is where omissions appear. Keeping the same standard across document, image, video, and audio redaction means a claim is treated consistently no matter what it contains.

The second is selective redaction that preserves usefulness. A reinsurer still needs the accident narrative. An offshore administrator still needs a complete, readable claim file to process it. Replacing every identifier with a solid black box can break those downstream workflows and push files back into manual review, which defeats the purpose. Removing the identity while keeping claim reference numbers, dates of loss, and risk-relevant facts intact lets a recipient do the job without ever learning who the policyholder is. The recipient gets a working file. The carrier sheds the liability.

The third is scale and consistency. A large carrier shares thousands of files a month, and a control that depends on individual judgment will drift over time. Batch processing and consistent detection rules keep the standard even across teams and volumes, so the hundredth file of the day is redacted to the same standard as the first. Files that go to legal counsel illustrate the point, since litigation production demands both completeness and careful removal of privileged or unrelated detail, a balance covered in our guide to redacting legal documents with AI.

What weak redaction looks like

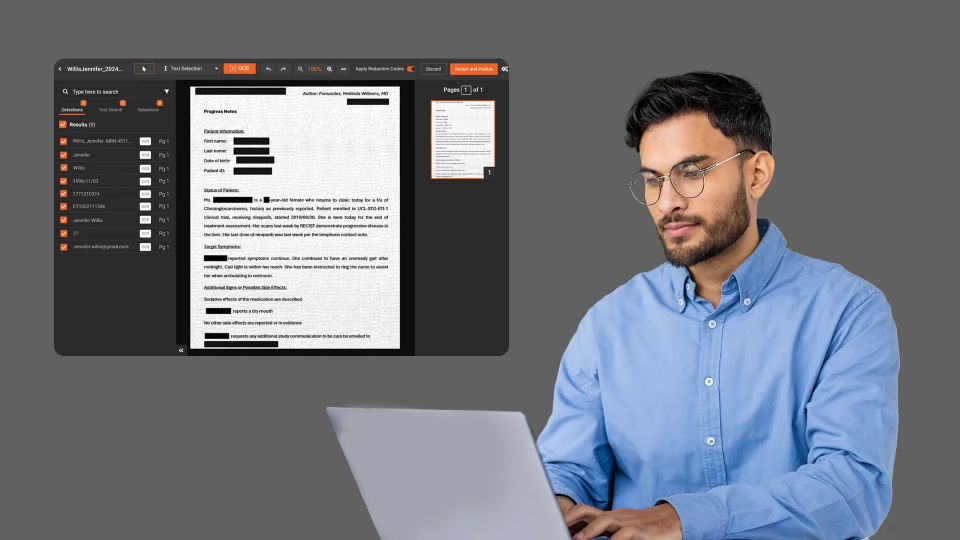

Not all redaction reduces risk, and the difference matters when a file is headed to a third party. The most common mistake is masking rather than removing. Drawing a black rectangle over text in a viewer often leaves the underlying characters intact in the document, recoverable by copy, search, or by opening a lower layer of the file. To the eye it looks redacted. To anyone willing to look closer, the data is still there.

Two other failures recur. Scanned and image-based files are treated as safe because the text is not selectable, when in fact the sensitive information is sitting in the image and needs optical character recognition to detect and remove. And embedded content inside a PDF, such as a photograph with a visible face or a license plate, is missed because the tool only inspected the text layer. Genuine redaction removes the information permanently, reads text inside images, and inspects embedded objects rather than only the page text. Anything short of that ships risk to a vendor while creating a false record that the file was cleaned.

VIDIZMO Redactor for insurance third-party risk

There is a quiet contradiction in much of the redaction market. Many tools promise to keep data safe before it is shared, yet they are themselves cloud services, so adopting one adds another vendor to the very network the carrier is trying to control, along with a fresh data-residency question. VIDIZMO Redactor can be deployed on-premise or in a private cloud, which means policyholder data can be sanitized inside the carrier's own environment without handing it to a new processor first.

Beyond deployment, Redactor brings the formats insurance evidence actually arrives in into one platform: documents, images, video, and audio, with OCR for scanned content and detection across a wide range of personal identifier types, including financial and medical identifiers and country-specific ones. It applies visual detection to objects embedded inside PDFs, not only the text layer, which matters for scanned claim packets and accident photographs.

It has been used for high-volume work, including bulk redaction of large recording and document libraries, which is the scale claims operations reach. Review workflows let a team validate accuracy before release, and audit logging supports the recordkeeping that compliance and litigation depend on.

Stop sending policyholder data into your vendor network unprotected. See how VIDIZMO Redactor removes sensitive information from claim files before they ever leave your environment.

About the Author

Jump to

Guide to Document Redaction Software for Automated Document Redaction

.webp)

How Insurance Companies Can Redact PII in Video & Audio Files

No Comments Yet

Let us know what you think